A blog where you can learn about property knowledge and get to know my latest New Launching Project in Klang Valley.

Monday, 19 December 2016

MRT Phase 2 almost 95% completed

PETALING JAYA (Dec 14): Progress-wise, the second and final phase of the Mass Rapid Transit (MRT) project involving the Semantan-Kajang line is almost 95% completed.

MRT Sungai Buloh-Kajang (MRT SBK) project director, Marcus Karakashian said progress includes all station structure works, rail systems and trains.

"We expect the MRT test run for the Phase Two to take place as early as January 2017 before its operation in July the same year," he told a media briefing here yesterday.

The 30km Phase Two involves 19 stations between Semantan to Kajang and part of the RM23 billion MRT project which spans 51km with 31 stations.

Meanwhile, Feeder Bus and Infrastructure Development chief Rudyanto Azhar said 112 feeder buses would begin operating on 25 routes from the 12 stations for the phase one, Sungai Buloh-Semantan line this Friday.

He said the buses would run on a frequency of between 10 minutes and 15 minutes with the routes designed to serve residential and commercial areas within 3 km of an MRT station.

Malaysia, Singapore ink deal on high-speed rail link

PUTRAJAYA (Dec 13): The agreement on the Kuala Lumpur-Singapore High-Speed Rail (HSR) was signed between Malaysia and Singapore today.

When completed, the HSR will slash travel time between KL and the island republic from over five hours by road to 90 minutes.

The 350km bullet-train line will "transform" the way the two do business, the countries' leaders said at the deal signing in Putrajaya, AFP reported today.

"I know people are excited about it," Malaysia Prime Minister Datuk Seri Najib Tun Razak said, adding the project would "open a new landscape in terms of bilateral relations".

Singapore Prime Minister Lee Hsien Loong described the rail link as a "marquee project" that will "transform the way we do business".

The deal was signed by Minister in the Prime Minister's Department Datuk Abdul Rahman Dahlan and Singapore Transport Minister Khaw Boon Wan.

Najib and Lee, who were attending the 7th Malaysia-Singapore Leaders’ Retreat here, witnessed the signing ceremony.

The price tag of the mega project is estimated to be as high as US$15 billion (RM67 billion) and is expected to be completed in 2026.

The trains will run at a top speed of more than 300kph.

The rail proposal has already sparked interest among major Chinese, Japanese, and South Korean rail firms.

Meanwhile, Bernama reported that the leaders of the two countries will not compromise on border security aspects in relation to the KL-Singapore HSR.

Najib said both countries had found ways to strike the right balance between being passenger friendly without overlooking security issues for the HSR.

"We have found the proper solutions. There will be three common customs, immigration and quarantine (CIQ) facilities. These will monitor movement of people.

"We believe it is a solution which is workable. It is passenger-friendly and at the same time does not compromise on the security aspects. I think we have found the right balance between the two," he said at a joint press conference with Lee here today.

Lee said there was a need to make the Malaysia-Singapore border safe and secure, Bernama reported.

"There is no need to close down the Malaysia-Singapore border due to security problems. We need to manage the problem with close cooperation from agencies on both sides,” he said at the same event.

Both governments will take responsibility for developing, constructing and maintaining the civil infrastructure and stations located in their respective countries.

The two countries have also agreed that the HSR will have eight stations, with terminals in Bandar Malaysia (Kuala Lumpur) and Singapore, and six intermediate stations in Putrajaya, Seremban, Ayer Keroh, Muar, Batu Pahat and Iskandar Puteri.

All stations will be designed to integrate with the local public transport systems to ensure seamless connectivity.

To facilitate swift and seamless travel, both governments also agreed to co-locate the CIQ facilities at three locations, namely Singapore, Iskandar Puteri and Kuala Lumpur, so that international-bound passengers will only need to undergo CIQ clearance by both Malaysia and Singapore authorities at the point of departure

“It is too secluded!”, “Why would you want to stay somewhere so inconvenient?”, “I’d rather stay in Bandar Mahkota Cheras”… These are among the most common responses we hear whenever Bandar Sungai Long is mentioned, while some have not even heard of the township before. Over the years, the impression formed of Bandar Sungai Long is remote, inconvenient, distant, and all things negative. But, is that really the case?

Originally a rubber estate, Bandar Sungai Long was developed into a township in 1989, which was only about 500 acres in size. Now, it covers about 690 acres! Due to changing market demands, new real estate projects have also been cropping up within the township, a telling sign of Bandar Sungai Long’s potential for growth.

Connectivity the catalyst for growth

Don’t be fooled by the expansive greenery surrounding Bandar Sungai Long - though it may feel like it’s miles away from the city, the township is in fact within easy connectivity to KL and other parts of the Klang Valley.

Highways connecting to this township include the Cheras-Kajang Expressway and the SILK highway, as well as a connecting road from the SILK highway that links directly to the residential area of Bandar Sungai Long (via Persiaran Bukit Sungai Long 1). Forget the hectic traffic of Bandar Mahkota Cheras, Bandar Sungai Long is accessible without having to brave through the crawl throughout the neighbouring towns during peak hours.

With these two connecting highways, heading to downtown KL will also be a breeze, with the SILK highway easily connecting to the SMART Tunnel, leading to KLCC within a few minutes. Under smooth traffic, residents can reach KLCC in approximately 25-30 minutes. Other than that, Semenyih is also within a 15-minute drive away via the SILK highway.

Connectivity to the region will further be improved with the East Klang Valley Expressway (EKVE) will be built and is slated for completion in 2019. By then, this 36.16 kilometers long highway will connect to Bandar Sungai Long, Bandar Mahkota Cheras, Hulu Langat, Ampang and Ukay Perdana, close to KL city. Apart from that, the EKVE will also enable easier connectivity to the Middle Ring Road 2 (MRR2) and DUKE highway. The upcoming EKVE is also set to bring a new facelift to Bandar Sungai Long.

In addition, Bandar Sungai Long is also included in the government's grand scheme for an improved and even more extensive public transportation system, with a total of four MRT stations planned within a 4km radius of the township. A combination of roadways and rail will enable increased connectivity from Bandar Sungai Long, with just a convenient hop onto the MRT which will bring commuters straight into the city centre. Rapid KL busses also serve the township of Bandar Sungai Long, providing ample accessibility within the town itself and to KL city for those without their own means of transportation.

Connectivity is the most essential element of urban living, which is not a difficult criteria for Bandar Sungai Long to fulfill.

Convenient living close to amenities

Though seemingly secluded from the world thanks to its peaceful environment,Bandar Sungai Long is a self-sustainable township, with residential and commercial developments within, complemented by commercial hubs and a great number of amenities necessary for convenient urban living.

Anchored by the exclusive Sungai Long Golf and Country Club (SLGCC), Bandar Sungai Long retains a quiet and peaceful surrounding, with acres of green turf and quaint lakes. SLGCC is aesthetically-appealing, however, given its world-class status, it may not be an easily affordable place for all to play. The course is the preferred spot for the Sultan of Selangor to enjoy a round of golf, as well as expatriates.

Amenities which can be found within Bandar Sungai Long are the basics like hospitals, petrol stations, markets, fitness centres and such, all within the township. Residents will not have to brave traffic or waste time driving too far in order to reach these much needed amenities.

Just 5 minutes from Bandar Sungai Long, is Bandar Mahkota Cheras, which provides a wide array of eateries, and entertainment spots. There is also an AEON Big hypermarket there, making it evermore convenient for residents of Bandar Sungai Long to acquire their daily necessities. There is also a night market every Tuesday along Persiaran Sungai Long 1, offering scrumptious street eats, drawing even those from nearby Bandar Mahkota Cheras and Kajang.

The nearest mall to Bandar Sungai Long is The Mines located in Seri Kembangan, just about 15 minutes away. The much larger IOI City Mall in Putrajaya is also only about 20 minutes away from the SILK highway that leads to the MEX highway before connecting to IOI City Mall.

As for educational institutions, aside from an existing secondary school, a brand new SJK (C) Bandar Sungai Long primary school has also begun recruiting students for the coming year. Since the establishment of the first block of Tunku Abdul Rahman University (UTAR) in August 2002, the university is now a 2-block campus in Sungai Long to accommodate more students and provide more facilities.

Variety of real-estate for a continuously booming community

The community of Bandar Sungai Long is a diverse one, ranging from families to single working professionals, to students, lecturers and staff of nearby UTAR, in addition to expats. As such, the property scene is a varied one, with residential developments of luxurious gated and guarded communities closer to the green fairways of the SLGCC to mid-range high-rise condominiums as well as semi-detached homes and terraces along with some commercial shop lots.

Most of the households in Bandar Sungai Long fall within the middle to high income group, with signs of gentrification as seen in the upgrading of security in the neighbourhoods. These older housing estates which were initially without security, are willing to pay for the construction of high-quality perimeter fencing and the employment of strict security teams to monitor their neighbourhoods. As such, most of the residential phases in Bandar Sungai Long has its own security.

Several high-rise residential developments are currently ongoing in the town, preparing to cater to the growing population of Bandar Sungai Long, set to change the skyline of the township by the time they are completed.

Untapped property market

According to data collected, it shows that most of the homebuyers who can afford to buy houses at Bandar Sungai Long belong to the middle to high income earning group, while buyers of newly-launched condominium projects in the area are mostly long-term residents currently living in the township itself.

Given the UTAR campus in the township, most of of the buyers are also those looking to buy to rent to students, and even staff and lecturers of the university. As such, these groups, both investors and renters, will provide a steady demand for properties in the township.

Properties in Bandar Sungai Long have relatively appreciated in value over the years. A standard double-storey terrace house which was RM550,000 ten years ago, can now fetch around RM1.3 million on the market, which is more than 100% of appreciation in value!

At present stage, the market demand for terrace units and apartments is considerably high, making it a great time to invest in these property types within the township; conversely, semi-detached and bungalow units are in lower demand, giving buyers a slight upper-hand. Thus, families or those who intend to settle down in Bandar Sungai Long should strongly consider buying a home now, so as not to miss out on the opportunity.

Bandar Sungai Long is also expected to be the second Petaling Jaya, given its proximity to the city and expanding population. Completion of the EKVE highway is also anticipated to spur more residential and commercial projects in the township.

Conclusion

By taking a closer look at Bandar Sungai Long, you may conclude that the general consensus of Bandar Sungai Long being “remote, faraway, and inconvenient” is a far cry from its strategic location. On the contrary, Bandar Sungai Long is close to several other established townships and enjoys direct access to major highways.

A unique township where you can be at one with nature while remaining close to the city, Bandar Sungai Long is a highly liveable township with a good choice of residential types where amenities and conveniences are just at your doorstep, while accessibility is a certainty given its strategic location.

Bandar Sungai Long is also a developing town, with future development plans for infrastructure and connectivity. As such, investors should keep an eye out on the area, where future developments will give potential for real-estate within the township to steadily rise.

Come watch this short video of Bandar Sungai Long:

OVERNIGHT POLICY RATE REDUCED !!!

13th July 2016, Bank Negara Malaysia (BNM) announced a drop of 25 basis points in the Overnight Policy Rate (OPR) in their bi-monthly Monetary Policy Meeting. Most analysts hold the opinion that the OPR should have been increased due to the impending increase of interest rates in the United States of America (USA). End of 2015 and earlier this year, I have been sharing my view with members that the OPR should be reduced in Q3 or Q4 2016, a prediction that has been materialized.

Overnight Policy Rate (OPR)

TheOPR is an interest rate/profit rate at which a bank lends to/receives from investment with another bank. OPR is determined by Bank Negara Malaysia (BNM) in the Monetary Policy Committee Meeting held throughout the year. In Malaysia, changes in the OPR trigger a chain of events that affect the Base Rate (BR), Base Lending Rate (BLR), short-term interest rates, fixed deposit rate, foreign exchange rates, long-term interest rates, the amount of money and credit, and, ultimately, a range of economic variables, including employment, output, and prices of goods and services ,which are the micro and macro effects on the economy.

The OPR has been trending at as low as 2% during the global financial crisis in 2009, and as high as 3.5% between 2006-2008. Below is the OPR trend for the past 10 years. Does this spark the start of an era of lower interest rates or is merely a one-off change? Before we discuss more on this, let us further understand the impact of the decrease of the OPR.

Source: Bank Negara Malaysia, July 2016

Impact of Reduced OPR

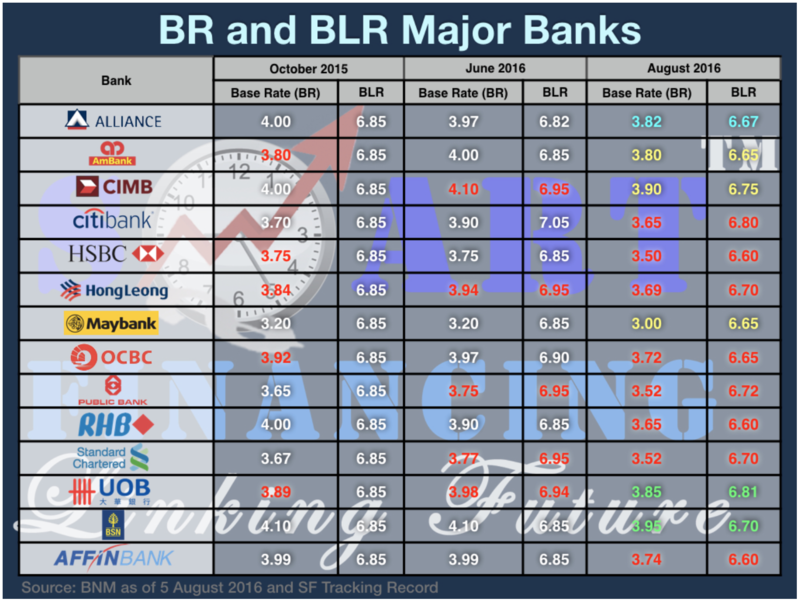

1. Influence on BR and BLR

There is a direct influence on the Base Rate (BR) and Base Lending Rate (BLR). When the OPR is reduced, it is stated in the Reference Rate Framework that BR and BLR will have to reduce in tandem of the OPR changes. This means reduction of OPR will directly reduce our effective lending rate (ELR) on existing loans which are using this floating rate. In other words, we are now charged with a cheaper interest rate. Below is the previous and latest BLR and BR rates:

2. Reduced instalment rate

Lowering the OPR reduces the ELR for existing loans, also meaning a lower instalment rate. This lower instalment will lead to better affordability to consumers as well. In banks, affordability is measured by the Debt Service Ratio (DSR), whereby the DSR will also reduce in view of lower interest rates. This means that now your affordability has increased and your chances of getting a loan approval are higher!

3. More profits for banks

However, this may not be good news for those who have yet to obtain a housing loan. It is foreseeable that most banks will be adjusting their spread with new BR loans offered to be similar or close to an ELR of 4.40% to 5.10%. This means now the banks stand to enjoy a better profit margin when giving out housing loans.

4. FD rates to follow suit

The rate of Fixed Deposits (FD) usually follow suit with the changes to the OPR. With a reduction of the OPR, FD rates set by banks have also lowered. This lower FD rate may prompt consumers to look for other alternative investment tools that can offer better returns. Consumer who do not take such actions may be impacted by the drop in deposit interest rates while in view that prices of goods and services might also continue to soar due to inflationary pressure, especially when the inflation rate is higher than 3%.

5. Higher spending power

As instalment rates reduce, this would mean that we can have additional cash on hand every month to spend in other aspects. This increases our spending power, which will potentially boost the economy.

6. Ringgit to weaken

In most instances, the OPR in other countries are normally used as a monetary policy tool to strengthen a country’s currency value. Hence, with the drop in the OPR by BNM, this would weaken the Ringgit against other currencies.

Must bank reduce my housing loan instalment amount?

In view of the reduction of BR and BLR by 14bps to 25bps (varying by bank) on the existing floating rate of housing loans, all banks are required to make adjustments to your monthly instalment, instead of making changes to your existing loan tenure. This is clearly stipulated in the BNM guidelines (as seen below). Even though by default, banks will be lowering your monthly instalment, they will normally give you the option to shorten your loan tenure instead of reducing the amount of monthly instalment you pay.

Conclusion

TheOPR reduction is certainly a good news to all. Though a reduction of interest rates was expected to weaken our Ringgit, the move had proved otherwise, where the Ringgit rallied against other major currencies after the announcement of the OPR reduction, while Bursa rebounded from negative territory as well. This demonstrates that most people are delighted with the change, and now you know, especially for ordinary home owners like you and me. It is certainly a pleasing fact that the amount of monthly instalment of our home loans are reduced, this also meaning we have can have more money to spend! Last but not least, BNM may further adjust the statutory reserve requirement towards the fourth quarter of 2016 and may possibly reduce the OPR again in the first quarter of 2017, which we shall look forward to seeing whether they do.

When we talk about buying a property, the first cost that comes to mind is always the initial down payment. But is that all? Aside from the down payment, there are other entry costs such as legal fees, stamp duty, valuation fees and real estate agent’s fee which are equally important, but usually neglected.

Here, we unveil to you the possible costs which you may incur when buying a property.

1. Down payment 10% of the total purchase price OR the difference between the loan amount and the purchase price

2. Costs related to S&P Agreement (Legal Fees + Stamp Duty)a. Legal Fees

Purchase Price Charge First 150,000 1.000% (subject to a minimum fee of RM300) Next 850,000 0.700% Next 2,000,000 0.600% Next 2,000,000 0.500% Next 2,500,000 0.400% Thereafter 0.300%

b. Stamp Duty or Memorandum Of Transfer

Purchase Price Charge First RM100,000 1.000% Next RM400,000 2.000% Thereafter 3,000% Note: As part of the Malaysian government's efforts to reduce the cost of ownership for first time home buyers, until 31 Dec 2014, for first time home buyers, there will be a 50% stamp duty discount on the instrument of transfer agreements and loan agreements for residential property purchases worth RM400,000 and below.

*Update: The new limit entitlement for the 50% stamp duty exemption is now for properties RM500,000 and below in accordance to Budget 2015. This will take effect starting 1st January 2015

3. Costs related to Loan Agreement (Legal Fees + Stamp Duty)a. Loan Legal Fees

The legal fee percentage and structure for loan agreement is similar to S&P legal fee structure. However, it will be based on the loan amount (unlike S&P that is based on the purchase price).

b. Stamp Duty / Loan Agreement

Loan Amount Charge Any Amount 0.500%

4. Valuation Fees (Where formal valuations are required)Valuation Charge First RM100,000 0.250% Next RM 1,900,000 0.200% Next RM5,000,000 0.167% Next RM 8,000,000 0.125% Next RM35,000,000 0.100%

5. Real Estate Agent’s Fee (Usually paid by the seller but may be charged to buyer instead)Purchase Price Charge Any Amount 3.000%

Conclusion There are people who make the mistake of underestimating the affordability before they make a purchase of a property. In most cases, it is the lack of knowledge regarding the hidden entry costs that causes complications.

A guide to some of the costs involved in buying a house ====================================================

If you are buying a house for the first time, the whole process of signing the Sale and Purchase agreement, dealing with solicitors, legal fees and stamp duty can be confusing. Here is a guide to some of the costs involved in buying a home.

How much can you afford?

A good rule of thumb to follow is that your monthly loan/financing instalments and current commitments (e.g. car loan, personal loan) should not exceed one-third of your monthly salary. Those who over-commit themselves financially may have difficulty making payments when emergencies crop up or if interest/profit rates rise.

Fixed or conventional rates?

A fixed interest/profit rate home loan/financing promises fixed instalments throughout the loan/financing tenure. It offers stability against fluctuating financing costs and ease of planning your monthly financial commitments.

A conventional loan/financing with variable interest/profit rates may suit those who want to take advantage of features such as overdraft facilities and so on.

Down payment

Generally, you will have to pay a booking or earnest fee of 2%-3% of the purchase price. This is non-refundable, so decide carefully before paying.

The bank usually finances up to 90% of the price of the property. You must have at least 10% in cash for the down payment. Also, don't forget that you can withdraw a limited amount from your EPF (Account 2) for your down payment.

Sale and Purchase agreement

Upon signing the Sale and Purchase agreement, you pay another 7%-8% of the purchase price, bringing the total down payment to 10% of the purchase price. After that, you usually have 3 months to pay up the balance or secure financing and a 1-month extension which is subject to 10% per annum interest/profit on the balance due.

If you are buying a property under construction, the developer generally appoints a lawyer to draw up the Sale and Purchase agreement. The bank will deal with the developer to make progressive payments on your behalf.

If you are buying a completed property, you need to engage a lawyer to advise and act on your behalf when signing the Sale and Purchase Agreement and making payments, until the transaction is completed.

Insurance/Takaful

As a home buyer, you will have to purchase Mortgage Reducing Term Assurance (MRTA) or Mortgage Reducing Term Takaful (MRTT), which ensures your home will be paid for in full should anything happen to you. The one-off premium payment is generally computed on the age of the borrower(s), loan/financing amount, tenure and interest/profit rate. It can be paid in cash up front or included in your loan/financing to minimise the initial cash outlay required.

Additionally, a Fire/House Owners Insurance/Home Building takaful policy is compulsory to protect your property against damage. Should a mishap occur, your insurance/takaful payments may be used to minimise losses. The premium is payable annually.

Stamp duty and legal fees

Stamp duties and legal fees will need to be paid for your Sale and Purchase Agreement and Loan/Financing Agreement.

Monthly instalments

To avoid late payment charges, it is best to pay your home loan/financing on time. If you miss several payments, you risk losing your home.

Other costs

Owning a place you can call home is a rewarding experience. After getting the keys to your home, however, there are still several other things you will have to pay:

Monthly service charges (if you own an apartment)

Deposits for utilities – TNB, JBA, Indah Water and telephone

Assessment (twice a year)

Quit rent (annually)

How to apply

Once you're ready to own a home, apply for a home loan/financing online with us in just 3 simple steps:

1. Application

Decide which home loan/financing is right for you. Click 'Apply now' and enter your personal details in the application form. If there is more than one applicant, you should submit their details too.

2. Processing

Print a copy of your application for your reference and then click "Submit" to send it to us.

3. Immediate response

If your application meets our initial requirements, your home loan/financing will be pre-approved immediately. You will receive a Provisional Letter of Offer and application reference number.

If the bank is unable to process your application for any reason, our Sales Officer will contact you within 3 working days.

Go to your selected Maybank branch within the next 14 days with a printout of the Provisional Letter of Offer and relevant documents for verification by the bank.

Important! The Provisional Letter of Offer is subject to confirmation of your details and credit eligibility. It does not include Mortgage Reducing Term Assurance (MRTA) or Mortgage Reducing Term Takaful (MRTT) which is compulsory. This will be calculated when you visit our branch and you may opt to pay it in a single payment or capitalise the sum into your loan/financing.

Checking your application online

You may check the progress of your loan/financing application online any time from 4am to 9pm. Select Pre-approved Home Loan/Financing Enquiry and key in your reference number. We will keep you informed from the time you apply for a loan/financing until the funds are fully disbursed.

How to Buy a House in Malaysia? ============================

For most people, the first taste of one's very own hard-earned income is indeed liberating. So, what comes next after being handed your first set of car keys? We certainly hope that your next goal would be to get another set of keys; one that opens the door to your very first own home!

Here's an abbreviated look at your possible path and checklist towards owning your first property.

1. INVEST IN YOURSELF FIRST Take a little time to meet and learn from experts, fellow investors and homebuyers.

2. KNOW AVERAGE PRICES House prices in Kuala Lumpur are the costliest in Malaysia with an average price of RM497,535.

3. BREAKDOWN OF EXPENDITURE Most financial experts recommend that you allocate no more than one-third of your total income to pay off your home loan. This is subject to your debt service ratio after including the new housing loan not exceeding 60% to maximum of 80%. Terms and conditions applied.

4. DETERMINE THE TYPE OF HOME What shall it be? Condominium, apartment, terrace house, semi-detached house or bungalow?

5. DO YOU HAVE ENOUGH FOR DOWN PAYMENT? For your first home, you need to put a down payment of 10% of your intended property's price. Generally, you will have to pay a booking or earnest fee of 2%-3% of the purchase price. This is non-refundable, so decide carefully before paying.

The bank usually finances up to 90% of the price of the property. You must have at least 10% in cash for the down payment. Also, don't forget that you can withdraw a limited amount from your EPF (Account 2) for your down payment.

6. HOW MUCH CAN YOU AFFORD? Take a hard look at what you are spending your money on and decide on a budget.

7. HOME LOAN INTEREST RATES The interest that banks charge will be determined by the Base Lending Rate (BLR) set by Bank Negara Malaysia (BNM).

8. ENGAGE A REAL ESTATE AGENT Tell them your requirements such as preferred locations, home type, unit size, loan tenure, land tenure and estimated budget.

9. MAKE AN OFFER You've found it! Once you and the seller have agreed on a purchase price, you will need to sign a standard document and pay the 2% earnest deposit. *For New Project, this is varies to the terms and conditions of the project.

10. GET A BANK LOAN Research the current packages and go for one that best suits your repayment profile. Visit your selected bank and apply for a housing loan. *This normally would be very incovenient for purchasers as purchasers normally have to work during office hours. Therefore I will arrange everthing for my purchaser. i will collect the required documents from purchaser, submit to few banks for my purchaser to compare the best rate offered among the banks. Banker will contact purchaser for the packages of loan their bank offer, explain in details and meet purchaser for signing LO. Thus my purchaser would in no need to worry about what to do next, I will keep updating purchaser until the end of the throughout process.

11. 3 WAYS TO LOWER YOUR MONTHLY INSTALLMENT a.) Place a bigger down payment. b.) Search for the lowest interest rate and packages. c.) Request for a longer loan period.

12. ADDITIONAL COSTS Apart from the down payment of 10%, there are other costs such as legal fees, 6% government service tax to be charged on the real estate agent's commission, stamp duty, and so on. *Subject to terms and condition.

13. CLOSING THE DEAL Once all the paperwork has been completed properly by your lawyer, you can make arrangements with the seller to get the keys to the property.

14. RENOVATE & CLEAN-UP Meet your contractors and interior designer, and submit your renovation plans.

15. MOVE IN! Pack up your stuff, move in and begin planning for a housewarming party!

Should you need further assistance, feel free to contact William 016-9322718

The Purchase Process for First-Time Home Buyers

==========================================

Purchasing your own property is generally an exciting time. However, it could prove to be a daunting affair as there are likely to be many questions in your mind. Here, we try to help you out with a simplified but important step-by-step guide towards your property purchase.

On top of that, there is a 5% government tax and approximately RM500 to RM1,000 disbursement cost. The disbursement cost covers the following:

• Stamping of Sales's Purchase Agreement (RM10 per copy x 4)

• Bankruptcy / Winding up search

• Company search (if applicable)

• Land search (before preparation of the SPA & prior to the filing of the Form 14A at the Land Office)

• Registration of Transfer at Land Office

• Affirmation on the Statutory Declaration to request for the 50% waiver on the stamp duty on the transfer/ on

• the assignment.

• Stamping on the Statutory Declaration to request for the 50% waiver on the stamp duty on the transfer/ on the assignment

Transportation

• Printing / facsimile / telephone / photocopy charges